Bankruptcy refiling is a common question potential clients ask. Can you refile a bankruptcy they ask. Yes, you can refile a bankruptcy. But the effect of a subsequent bankruptcy filing varies depending on how long it has been since you last filed bankruptcy. It also depends on how the prior bankruptcy concluded. Was the prior bankruptcy case concluded successfully? Did it result in a bankruptcy discharge, or was it dismissed. When a bankruptcy case is completed, and all goes well, the result is a discharge. A bankruptcy discharge eliminates your debt. With a Chapter 7 bankruptcy normally all your debt is discharged. In a Chapter 13 bankruptcy you commonly pay a portion of your debt, and then discharge what you cannot afford to pay. But if a case is dismissed, a discharge is not ordered by the bankruptcy court.

Refiling OptionsRefiling after a prior case was dismissed is common, and can usually be filed right after the prior case is dismissed. A bankruptcy refiling after the previous case was discharged may result in another discharge, or it may not. It depends how long between the bankruptcy filings.

If it has been 8 years since your last case was filed, all bankruptcy options should be available again. If more more than 4 years but less than 8, you can file a Chapter 13 bankruptcy and discharge what you can't afford to pay; but you will need to pay something in that situation, even if only 1% of your debt. Less than 4 years you normally do not get a discharge. But you can refile a bankruptcy and get bankruptcy protection, provided you repay all your debt. This is a common scenario for those facing a home foreclosure. If their home is being foreclosed and they filed bankruptcy resulting in a discharge the last 4 years, they can still stop the foreclosure process with a bankruptcy filing. But they would have to pay back their debt owed on the house and other debts.

Bankruptcy Refiling RisksThough bankruptcy refiling can be an option, it can come at a cost. If you file bankruptcy and have had a prior case pending in the prior year, you only get 30 days of bankruptcy protection. You have to ask the court for more if you need it. Two prior cases in the past year is even worse. You get no bankruptcy protection under that circumstance. You have to ask the judge to order it to get it. There are restrictions and technical rules to it all. Best if you don't have to refile. But it is nice to know you can if you have to.

Contact me for a free consultation if you have any questions concerning bankruptcy refiling. It is a very technical area of bankruptcy law that is best not done without professional advice. The Sacramento Bankruptcy Court is another good option for information you may need.

Normally a bankruptcy plan is initiated with the filing of a Chapter 13 bankruptcy. The Chapter 13 plan will provide the terms of your debt repayment. Both businesses and individuals can file. It will list how much you will pay back. For how long you will repay your creditors. And it will include who you will repay. News of the bankruptcy of ‘American Idol’ producers’ debts were disclosed in a bankruptcy repayment plan.

Normally a bankruptcy plan is initiated with the filing of a Chapter 13 bankruptcy. The Chapter 13 plan will provide the terms of your debt repayment. Both businesses and individuals can file. It will list how much you will pay back. For how long you will repay your creditors. And it will include who you will repay. News of the bankruptcy of ‘American Idol’ producers’ debts were disclosed in a bankruptcy repayment plan. Not everyone is eligible to file bankruptcy. But those who are can eliminate, or discharge, their debts thought a bankruptcy filing. Limitations exist that may prevent some from filing bankruptcy and receiving a bankruptcy discharge. These impediments to a bankruptcy discharge may be previous bankruptcy filings, excess income or too much property. If eligible, though, a bankruptcy discharge order will result from a bankruptcy filing and successful case completion.

Not everyone is eligible to file bankruptcy. But those who are can eliminate, or discharge, their debts thought a bankruptcy filing. Limitations exist that may prevent some from filing bankruptcy and receiving a bankruptcy discharge. These impediments to a bankruptcy discharge may be previous bankruptcy filings, excess income or too much property. If eligible, though, a bankruptcy discharge order will result from a bankruptcy filing and successful case completion. Credit availability is, obviously, tied to debt. And credit availability is now back. Much of credit market dried up during the great recession in years past. Now credit is back. So is debt. And along with it the need for debt relief. There is no more comprehensive or complete recovery from debt than filing for bankruptcy. Again, that is why you are not alone filing bankruptcy.

Credit availability is, obviously, tied to debt. And credit availability is now back. Much of credit market dried up during the great recession in years past. Now credit is back. So is debt. And along with it the need for debt relief. There is no more comprehensive or complete recovery from debt than filing for bankruptcy. Again, that is why you are not alone filing bankruptcy. Qualifying for Chapter 7 bankruptcy requires the filer to pass the bankruptcy means test. This, then, is the primary bankruptcy means test meaning. To “pass” the bankruptcy means test, the filer must demonstrate eligibility to file for Chapter 7 bankruptcy. What this means is that an individual or couple filing for Chapter 7 bankruptcy must prove eligibility for a Chapter 7 filing. To be eligible for filing Chapter 7 bankruptcy, filers must show, essentially, their living expenses exceed their income. Put another way, they owe more in living expenses than income earned. This recent news article clarifies many of the bankruptcy means tests basics.

Qualifying for Chapter 7 bankruptcy requires the filer to pass the bankruptcy means test. This, then, is the primary bankruptcy means test meaning. To “pass” the bankruptcy means test, the filer must demonstrate eligibility to file for Chapter 7 bankruptcy. What this means is that an individual or couple filing for Chapter 7 bankruptcy must prove eligibility for a Chapter 7 filing. To be eligible for filing Chapter 7 bankruptcy, filers must show, essentially, their living expenses exceed their income. Put another way, they owe more in living expenses than income earned. This recent news article clarifies many of the bankruptcy means tests basics. Though bankruptcy is an initial negative on your credit after you file, discharging your debts at the conclusion of your bankruptcy is a big benefit. How big that benefit is to you depends on the amount of debt your discharged, or eliminated. By weighing the cost of the bankruptcy impact versus the discharged debt is the essential evaluation of whether to file for bankruptcy. If you have big debt and little income, bankruptcy may be a good option for you. If, though, your debt is not too great and your income enough to handle that debt, maybe bankruptcy is not your best bet. Every situation is different.

Though bankruptcy is an initial negative on your credit after you file, discharging your debts at the conclusion of your bankruptcy is a big benefit. How big that benefit is to you depends on the amount of debt your discharged, or eliminated. By weighing the cost of the bankruptcy impact versus the discharged debt is the essential evaluation of whether to file for bankruptcy. If you have big debt and little income, bankruptcy may be a good option for you. If, though, your debt is not too great and your income enough to handle that debt, maybe bankruptcy is not your best bet. Every situation is different. Your income, including your income history, is required as part of the bankruptcy process. Eligibility for certain bankruptcy filings, including both Chapter 7 & 13 filings, depend on the amount of income you earn. To file for Chapter 7 bankruptcy, your income must be lower than your expenses. For a Chapter 13 bankruptcy your must earn more than you spend. Whatever bankruptcy option you need, you must disclose accurate financial facts.

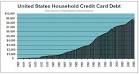

Your income, including your income history, is required as part of the bankruptcy process. Eligibility for certain bankruptcy filings, including both Chapter 7 & 13 filings, depend on the amount of income you earn. To file for Chapter 7 bankruptcy, your income must be lower than your expenses. For a Chapter 13 bankruptcy your must earn more than you spend. Whatever bankruptcy option you need, you must disclose accurate financial facts. If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done.

If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done. Posting pictures of property you did not disclose in a bankruptcy filing on social media is a really bad bankruptcy bad idea. Rapper 50 Cent may have put himself in this spot. Recently he posted on social media pictures of him surrounded by piles of cash. 50 Cent is in an active bankruptcy case now. If he did not disclose this money in his filing, he may be in big trouble.

Posting pictures of property you did not disclose in a bankruptcy filing on social media is a really bad bankruptcy bad idea. Rapper 50 Cent may have put himself in this spot. Recently he posted on social media pictures of him surrounded by piles of cash. 50 Cent is in an active bankruptcy case now. If he did not disclose this money in his filing, he may be in big trouble. Refiling a bankruptcy often comes with a penalty. To prevent people from filing too many bankruptcies, particularly in quick succession, Congress imposed restrictions on later filings to inhibit them. If, for whatever reason (and there can be many), you do need to refile a bankruptcy, it can be done. Usually, too, there is no penalty for doing so, especially if the cases are spread broadly over time. But if someone files bankruptcy 3 times in year, there likely would be problems. By being able to convert your case, you eliminate possible problems with future bankruptcy needs.

Refiling a bankruptcy often comes with a penalty. To prevent people from filing too many bankruptcies, particularly in quick succession, Congress imposed restrictions on later filings to inhibit them. If, for whatever reason (and there can be many), you do need to refile a bankruptcy, it can be done. Usually, too, there is no penalty for doing so, especially if the cases are spread broadly over time. But if someone files bankruptcy 3 times in year, there likely would be problems. By being able to convert your case, you eliminate possible problems with future bankruptcy needs.