Title Loans in Bankruptcy

Title loans in bankruptcy are a common connection. And for good reason. Title loans, commonly called pink slip loans, cost. They cost a lot! Title loan interest rates can reach nearly 400%.

Title loans use the equity in your vehicle as collateral for a loan. You do not have to own your car outright. But you have to have more equity in it than the loan you take. Repaying the loan is tougher than taking it out. With high interest rates come high repayments. As with payday loans, repaying title loans often involves taking out other loans to make the payments. This is a common cause why title loans in bankruptcy are common. And it is the cause why the government is now reconsidering the regulation of auto title loans and payday loans.

This USA Today story reflects the government’s potential coming crackdown on these loans. Title loans in bankruptcy are a sign that these debts can be bad news. Payday loans certainly are, and are even more prevalent in bankruptcy filings. There is, though, still an argument in favor of title and payday loans. And it stems from the same groups that most commonly discharge

This USA Today story reflects the government’s potential coming crackdown on these loans. Title loans in bankruptcy are a sign that these debts can be bad news. Payday loans certainly are, and are even more prevalent in bankruptcy filings. There is, though, still an argument in favor of title and payday loans. And it stems from the same groups that most commonly discharge

Often consumers want to repay part of their debt. Though a bankruptcy discharge of

Often consumers want to repay part of their debt. Though a bankruptcy discharge of Though bankruptcy is an initial negative on your credit after you file, discharging your debts at the conclusion of your bankruptcy is a big benefit. How big that benefit is to you depends on the amount of debt your discharged, or eliminated. By weighing the cost of the bankruptcy impact versus the discharged debt is the essential evaluation of whether to file for bankruptcy. If you have big debt and little income, bankruptcy may be a good option for you. If, though, your debt is not too great and your income enough to handle that debt, maybe bankruptcy is

Though bankruptcy is an initial negative on your credit after you file, discharging your debts at the conclusion of your bankruptcy is a big benefit. How big that benefit is to you depends on the amount of debt your discharged, or eliminated. By weighing the cost of the bankruptcy impact versus the discharged debt is the essential evaluation of whether to file for bankruptcy. If you have big debt and little income, bankruptcy may be a good option for you. If, though, your debt is not too great and your income enough to handle that debt, maybe bankruptcy is Since a wage garnishment is a form of a court order, it is often imposed involuntarily. You don’t have to allow a garnishment. It is placed there whether you want it or not. Facing such a situation, bankruptcy and wage garnishments often intertwine. Why? Because bankruptcy will stop a garnishment.

Since a wage garnishment is a form of a court order, it is often imposed involuntarily. You don’t have to allow a garnishment. It is placed there whether you want it or not. Facing such a situation, bankruptcy and wage garnishments often intertwine. Why? Because bankruptcy will stop a garnishment. When it comes to debt, beware is often overlooked. Too frequently debt plays too intimate a role in our daily lives. And so with it goes the cost. The costs of debt to consumers can be crippling. And often it is. What, then, to do?

When it comes to debt, beware is often overlooked. Too frequently debt plays too intimate a role in our daily lives. And so with it goes the cost. The costs of debt to consumers can be crippling. And often it is. What, then, to do? Your income, including your income history, is required as part of the bankruptcy process. Eligibility for certain bankruptcy filings, including both Chapter 7 & 13 filings, depend on the amount of income you earn. To file for Chapter 7 bankruptcy, your income must be lower than your expenses. For a Chapter 13 bankruptcy your must earn more than you spend. Whatever bankruptcy option you need, you must disclose accurate financial facts.

Your income, including your income history, is required as part of the bankruptcy process. Eligibility for certain bankruptcy filings, including both Chapter 7 & 13 filings, depend on the amount of income you earn. To file for Chapter 7 bankruptcy, your income must be lower than your expenses. For a Chapter 13 bankruptcy your must earn more than you spend. Whatever bankruptcy option you need, you must disclose accurate financial facts. It is common for people to be overpaid by the EDD and SSA for unemployment and other benefits. Millions of people file for and receive such benefits. Instruction and oversight covering the application for these benefits, though, is slight. Sometimes the money paid does not match the benefits earned. When the EDD or SSA finds out, debt can result. The EDD even has a link on their website concerning overpayments. But again, bankruptcy can discharge the overpayment of unemployment and Social Security Benefits.

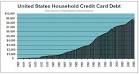

It is common for people to be overpaid by the EDD and SSA for unemployment and other benefits. Millions of people file for and receive such benefits. Instruction and oversight covering the application for these benefits, though, is slight. Sometimes the money paid does not match the benefits earned. When the EDD or SSA finds out, debt can result. The EDD even has a link on their website concerning overpayments. But again, bankruptcy can discharge the overpayment of unemployment and Social Security Benefits. If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done.

If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done.