Bankruptcy Can Discharge Overpayment of Unemployment and Social Security

Bankruptcy can discharge overpayment of unemployment and Social Security benefits. Like any other unsecured debt, such benefit overpayments are legally binding. But as with most other legally binding debts, bankruptcy can discharge them. There is no special provision in the law that denies the dischargeability of these debts. So if you are overpaid unemployment from the California Employment Development Department (EDD), or benefits from the Social Security Administration (SSA), you can eliminate these debts through bankruptcy.

It is common for people to be overpaid by the EDD and SSA for unemployment and other benefits. Millions of people file for and receive such benefits. Instruction and oversight covering the application for these benefits, though, is slight. Sometimes the money paid does not match the benefits earned. When the EDD or SSA finds out, debt can result. The EDD even has a link on their website concerning overpayments. But again, bankruptcy can discharge the overpayment of unemployment and Social Security Benefits.

It is common for people to be overpaid by the EDD and SSA for unemployment and other benefits. Millions of people file for and receive such benefits. Instruction and oversight covering the application for these benefits, though, is slight. Sometimes the money paid does not match the benefits earned. When the EDD or SSA finds out, debt can result. The EDD even has a link on their website concerning overpayments. But again, bankruptcy can discharge the overpayment of unemployment and Social Security Benefits.

The only limitation to bankruptcy being able discharge overpayment of unemployment and Social Security benefits is fraud. If excess benefits are obtained from false information, bankruptcy will not help. Understandably, only overpayment

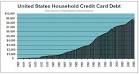

If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done.

If, just considering the average credit card debt, the amount spent on interest in a few months is more than the cost of filing a bankruptcy, there is bankruptcy bang for the buck. It is easy to see why. Spending $1,500 filing for bankruptcy is less than the interest you pay on your credit cards over a few months. Spending money on your credit card interest gets you nowhere. Filing bankruptcy gets you a discharge and your debt is done. College costs have exploded and, along with it, debt. College degrees, once considered financial bedrock, have not held their value compared to their costs. If your graduate from college you should earn more. Right? Often this is not so. At least when it comes to the inflated costs to get the degree. Earning $1,000 more per month does little good if that comes with a lifetime debt of $1,200 per month. The math doesn’t make sense. Perhaps, then, now is the time to evaluate whether you should be able to discharge

College costs have exploded and, along with it, debt. College degrees, once considered financial bedrock, have not held their value compared to their costs. If your graduate from college you should earn more. Right? Often this is not so. At least when it comes to the inflated costs to get the degree. Earning $1,000 more per month does little good if that comes with a lifetime debt of $1,200 per month. The math doesn’t make sense. Perhaps, then, now is the time to evaluate whether you should be able to discharge Posting pictures of property you did not disclose in a bankruptcy filing on social media is a really bad bankruptcy bad idea. Rapper 50 Cent may have put himself in this spot. Recently he posted on social media pictures of him surrounded by piles of cash. 50 Cent is in an active bankruptcy case now. If he did not disclose this money in his filing, he may be in big trouble.

Posting pictures of property you did not disclose in a bankruptcy filing on social media is a really bad bankruptcy bad idea. Rapper 50 Cent may have put himself in this spot. Recently he posted on social media pictures of him surrounded by piles of cash. 50 Cent is in an active bankruptcy case now. If he did not disclose this money in his filing, he may be in big trouble. The incident has certainly garnered attention, as this Wall Street Journal article reflects. Being in bankruptcy obligates a debtor such as 50 Cent to comply with the mandates of bankruptcy law. In exchange, he is entitled to bankruptcy protection. This includes prevention of collection efforts and lawsuits from creditors. One such creditor suit in Mr. Jackson’s bankruptcy is from a sexual

The incident has certainly garnered attention, as this Wall Street Journal article reflects. Being in bankruptcy obligates a debtor such as 50 Cent to comply with the mandates of bankruptcy law. In exchange, he is entitled to bankruptcy protection. This includes prevention of collection efforts and lawsuits from creditors. One such creditor suit in Mr. Jackson’s bankruptcy is from a sexual Like other forms of debt that can’t be afforded, bankruptcy may be a solution. Health insurance holes are a cause of potential debt. Like credit card debt, car repossessions or other unsecured debt, medical bills may prompt consumer bankruptcy. Unlike other forms of debt, though, medical care costs often come with a higher price tag.

Like other forms of debt that can’t be afforded, bankruptcy may be a solution. Health insurance holes are a cause of potential debt. Like credit card debt, car repossessions or other unsecured debt, medical bills may prompt consumer bankruptcy. Unlike other forms of debt, though, medical care costs often come with a higher price tag. Paying only minimum payments will get you nowhere. It’s only financial benefit is to the credit card industry. Using this

Paying only minimum payments will get you nowhere. It’s only financial benefit is to the credit card industry. Using this  Bankruptcy is a financial tool to del with your debt. Maybe you file bankruptcy because you can’t afford any of it. Maybe you file because you can only pay part of it. An maybe, why Kanye West may be filing bankruptcy, you do it because you need to rearrange your debt to manage it. There are many reasons to file for bankruptcy.

Bankruptcy is a financial tool to del with your debt. Maybe you file bankruptcy because you can’t afford any of it. Maybe you file because you can only pay part of it. An maybe, why Kanye West may be filing bankruptcy, you do it because you need to rearrange your debt to manage it. There are many reasons to file for bankruptcy.